Neighbor News

The 5 Credit Essentials That Will Reward You Handsomely

Becoming savvy with your credit can save you tens of thousands of dollars as a homeowner in the long run.

Are you a potential home buyer thinking of starting on your home buying journey? Are you a homeowner who may want to refinance at some point? Do you have a family member or friend looking to buy a home or refinance soon? Becoming savvy with your credit data when applying for a mortgage loan is extremely essential. Why? At the very least it’ll save you unexpected surprises, or even heartache during your home buying or refinancing journey. At the highest level, you’ll save yourself tens of thousands of dollars over the long-run.

Understanding Credit and the Two Major Scoring Models

At a basic level, your credit score represents your creditworthiness – your track record of how you manage and repay your outstanding debt. Your debt may consist of a mortgage loan, car loan(s), credit cards, student loans and/or medical bills. All lending institutions use your credit score as one of the key factors to determine your overall risk profile. This assessment allows lenders the confidence they need to approve or decline your request for a loan. Your credit score will fall in the range of 300 to 850.

Find out what's happening in San Ramonfor free with the latest updates from Patch.

There are many credit scoring models that provide credit scores these days, The two most heavily used models are the FICO score (Fair Issac Corporation) and the VantageScore. Both models provide different credit scores for the same borrower. This is because both models use their own proprietary algorithms to determine the credit scores.

When applying for a mortgage loan, take note that conventional, Federal Housing Administration (FHA), Veterans Affairs (VA) and most non-conventional mortgage (jumbo loan) lenders onlyaccept FICO scores. For purposes of our discussion on credit required to apply for a mortgage loan, we will use the FICO score.

Your credit-related data used to calculate the FICO score (also the VantageScore and other credit scoring models) comes from Experian, Equifax, and Transunion. These are the three biggest credit reporting bureaus in the U.S.

Find out what's happening in San Ramonfor free with the latest updates from Patch.

Tip: When shopping for a great deal on a mortgage loan make sure you are using a credit report with a FICO score. Most online websites providing free credit reports like the federally mandated annualcreditreport.com, Credit Karma, and others use VantageScore. You may even have a recent credit report that was used to purchase a car or originate other kinds of debt. These credit reports and scores do not apply when you are trying to secure a mortgage loan. Your FICO credit report costs a small fee (around $25 – $30) and your score is valid for 90 days.

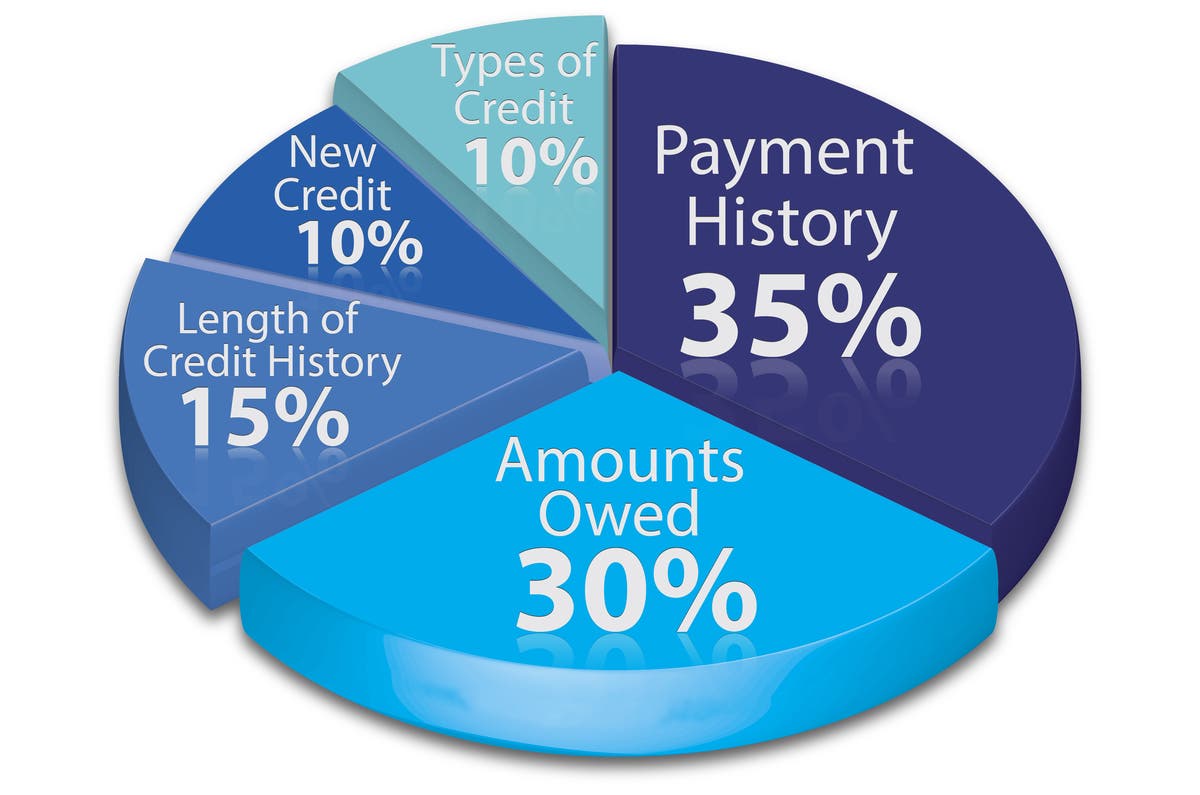

The Key Ingredients of FICO Score

FICO scores range between 300 to 850. The graph below breakdowns the five main factors that make-up your FICO score, including each factor’s impact on your score.

Tip: To maintain a healthy FICO score, all you really need to do is to keep your payment history clean and consistent, the amount you owe on each of your outstanding loans low (the amount you owe should be equal to or less than 30% of the maximum limit on your loan), and have a minimum credit history of two years. The combination of these three factors makes up for 80% of your FICO score.

Having a strong understanding of what makes up your credit profile and how to build a healthy score is particularly important for millennials and all first-time home buyers as you plan to acquire your biggest asset – you home, as well as, your biggest liability – your mortgage loan.

The Credit Score That Really Matters

As noted earlier, your credit data used to calculate your FICO score comes from Experian, Equifax, and Transunion. Your credit score reported by each of the three credit bureaus will be different. This is because your credit information captured and stored by each bureau is slightly different. Therefore, in essence, you have three distinct credit scores – one unique score from each of them.

Example: Your FICO scores from the three bureaus may be as follows: Experian = 709; Equifax = 721; Transunion = 730. Lenders take the middle of the three scores to determine your qualifying FICO score. In this example, your FICO score is 721.

If you have a co-applicant on the mortgage loan with you, the same process applies to them. Let’s assume your co-applicant’s middle score is 718. Lenders will use the lower of the two applicants score to base their decision on. In this case, the qualifying FICO score is 718.

Tip: If a co-applicant has a lower score that may adversely impact your loan approval or get you a higher interest rate, consider removing the co-applicant. This decision becomes easy if the co-applicant’s income is not needed to get approved for the loan.

The Impact of a Good Score

Mortgage lenders base their all-important loan approval, loan program, interest rate decisions on your FICO score. Lenders have their own unique credit scoring ranges. They use these specific ranges to determine whether you get approved for a particular loan program and/or interest rate.

Here, we use our on-going loan origination experience across the best lenders in the United States to create this FICO score matrix for your reference. This matrix lays out the general FICO score ranges and how lenders are using these ranges to providing loan programs and mortgage rates.

| Credit Score | Rating | Importance of Your Credit Score |

| 300-579 | Poor | Potential homebuyers in this credit score range will not qualify for a mortgage loan. It is highly advised for borrowers in this range to seek the advice of an experienced mortgage advisor and credit consultant. |

| 580-619 | Fair | Homebuyers with scores in this range are considered ‘subprime’ borrowers. You will only qualify for a FHA or VA loan program with a credit score in this credit score range. FHA loans require upfront and ongoing mortgage insurance to protect against borrower default. The VA loan requires an VA loan fee. |

| 620-679 | Good | Conventional lenders need at least a 620 score to qualify homebuyers on any of their loan programs. |

| 680-719 | Very Good | Homebuyers have access to better rates and more loan programs, including non-conforming/jumbo loans and adjustable rate mortgages with higher loan amounts. You need a minimum credit score of 700 to qualify for a jumbo loan. According to myfico.com, Americans had an average score of 700 as of April, 2017. |

| 720-739 | Excellent | Homebuyers with scores in this range will receive competitive rates and are likely to qualify for many of the low down payment loan programs from non-conventional (jumbo) lenders. Homeowners with a jumbo loan can also expect competitive rates and low closing costs. |

| 740-850 | Exceptional | Homebuyers with scores at or above this threshold qualify to receive the best mortgage rates and terms, as well as, the lowest down payment loan programs available from both conventional and non-conventional lenders. Homeowners looking to refinance their mortgage can expect the best rates and lowest closing costs with a credit score in this range. |

Highlights from the FICO score matrix above are summarized as follows:

Choice of Loan Programs: Higher FICO scores give you a wider range and better options for loan programs to choose from.

Cost of Capital: Higher FICO scores allow you a lower mortgage interest rate. The total costs associated with higher scores are also significantly lower. The combination of lower rates and closing costs will result in significant savings for you over the lifetime of the loan.

Example: On a conventional 30-year fixed loan, assuming 20% down payment, the difference in the interest rate on a score of 640 vs 720 can be between 75 basis points (bps or .75%) and 100 bps (1.0%). The payment difference on a $500,000 loan amount will be $226 per month. And, if you add up the principal and interest payments made over the lifetime of the loan, you will be paying a whopping $81,000 (rounded to the nearest $1,000) more with a lower FICO score. This example assumes that the closing costs are the same for both FICO scores.

One Thing More Important Than Your Score

You may have a solid FICO score currently. However, your FICO score can shadow some key insights in your personal credit history. Lenders are mindful of that. Hence, lenders focus their review on something more important than your score – your credit profile.

Here are some landmines in your credit profile that you need to prepare for or be careful about. These tips are especially pertinent for millennial home buyers.

Number of Trade-Lines: You are required to have at least three trade-lines that are currently open.

Credit History: You must have a credit history of at least two years. Most lenders will require you to have the minimum number of trade-lines open for two years.

Delinquencies: A serious delinquency in your recent past may adversely impact your ability to get a mortgage. Seriously delinquencies include bankruptcy, foreclosure, short-sale, collection(s) or judgment. You will need to wait for an allocated time-period and maintain a stable credit history before lenders will approve you. Relatively smaller delinquencies can also severally impact your ability to qualify for a mortgage loan. Examples would be a late payment on your mortgage, your credit card, and/or other consumer debt payments.

Conclusion

It pays handsomely to have a solid FICO score before you start your home buying or refinancing journey. Your credit report contains extremely important information about your ability to qualify and get approved on your home loan. In addition, the interest rate you receive and the loan program you can choose is directly related to your FICO score.

It is recommend that you start by having a seasoned mortgage advisor pull and review your FICO credit report. Your mortgage advisor will guide you through any correctional steps you need to take to build, improve, or even fix your FICO score. This crucial action you take upfront will save you any surprises later when you officially start your mortgage loan process. We hope that these credit tips for homebuyers and homeowners enable you to save money immediately, and reap major dividends in the long-run.

At Reliance Financial we are committed to bringing you the latest information that may enable you to make more informed decisions when it comes to buying and/or selling your residential Real Estate. For more information or to check mortgage rates on a home loan, you can connect with one of our advisors at www.RelianceFinancial.com, email us at info@reliancefinancial.com or call us at 925-236-9501.