Politics & Government

GOP Health Care Plan: Elderly Take Brutal Hit — And 40 Is Now Elderly

If you're 40 or older, you may not be able to afford your health insurance once Obamacare goes away.

Editor's Note: Senate Republicans are hard at work on a replacement health care program that would affect millions of Americans in profoundly different ways. Among the hardest hit would be middle-class people ages 40 to 64.

Patch Miami editor Paul Scicchitano explores how this critical legislation will affect the lives of real Americans in this group and finds that millions of people would lose their insurance altogether while the cost of premiums could skyrocket by tens of thousands of dollars. This story was updated to reflect Monday's analysis by the Congressional Budget Office.

MIAMI, FL — At age 60, diabetes has taken one of Stephen Cody’s toes. The former trial attorney was already battling diminished vision from an unrelated condition: Two gel-like membranes in the back of his eyes pulled away from his retinas, with sudden cruelty, plunging him into a world of murky shadows as he sat in rush-hour traffic.

Find out what's happening in Miamifor free with the latest updates from Patch.

For all his education and life experience, no one ever told Cody that aging would be such a bitch.

“That nearly blinded me for a while. I was looking around two huge things like tentacles — squids that had just sort of drifted down into my vision,” he recalled. With time, his eyesight improved enough that he could once again drive himself around his Miami suburb, but not enough to read the crag of documents generated by a successful law practice. “What I’m left with looks kind of like lace curtains flowing as I move my eyes around.”

Find out what's happening in Miamifor free with the latest updates from Patch.

See also: Senate Health Care Plan: Likely To Add Billions Of Dollars In Uncovered Expenses For Hospitals

Watch: Senate GOP Health Bill Plans Big Cuts To Medicaid

Even so, Cody considers himself blessed compared to many Americans his age.

Since 2014, he has waged his health battle with a bounce from the safety net of Obamacare, a program that protects his life savings and — until recently — had given him financial peace of mind. Each month he pays $329.88 to maintain insurance coverage for himself, his wife and two children. Most prescriptions and regular doctor visits cost only $5.

In recent days, that peace of mind has given way to an unsettling thought: Republicans intent on ending Obamacare could soon pass legislation that would increase his insurance costs by thousands of dollars a year.

Senate Republicans plan to vote by Thursday on their version of heath care reform in a bill that has become the guiding document for the full Congress.

Whether any repeal of Obamacare can pass Congress is in doubt. What is certain is this: if either of the current plans make it into law, millions more people will join the ranks of the uninsured, and older Americans — "older" in this case meaning as young as 40 — will be among those hit hardest.

Secret Drafting Committee

Only a handful of Republican senators were invited by Senate Majority Leader Mitch McConnell to craft the proposed legislation they released on Thursday.

“The average Republican doesn't even know what's in that legislation,” former Democratic presidential candidate Bernie Sanders jabbed at his GOP rivals on “Face the Nation,” only a few days before the document was released.

Forced to Gamble

There is little question that health insurance will almost certainly cost more and cover less for older Americans like Cody, who are too young for Medicare and too old to qualify for affordable health care. In the case of diabetics and people with other health problems, premium increases will likely be so steep that many will literally be forced to bet their lives on the hope they can outrun serious illness.

Some will most certainly lose that gamble.

About 3 million people between the ages of 50 and 64 — the age group hardest hit under the Senate plan — now buy their insurance under Obamacare, while some 8 million people between the ages of 45 to 64 qualify for health care under Medicaid.

Under the Senate plan, not only would those people see their insurance costs increase for policies that cover less, people as young as 40 would pay more because they would be lumped in with the more traditional definition of elderly, those 50 and older.

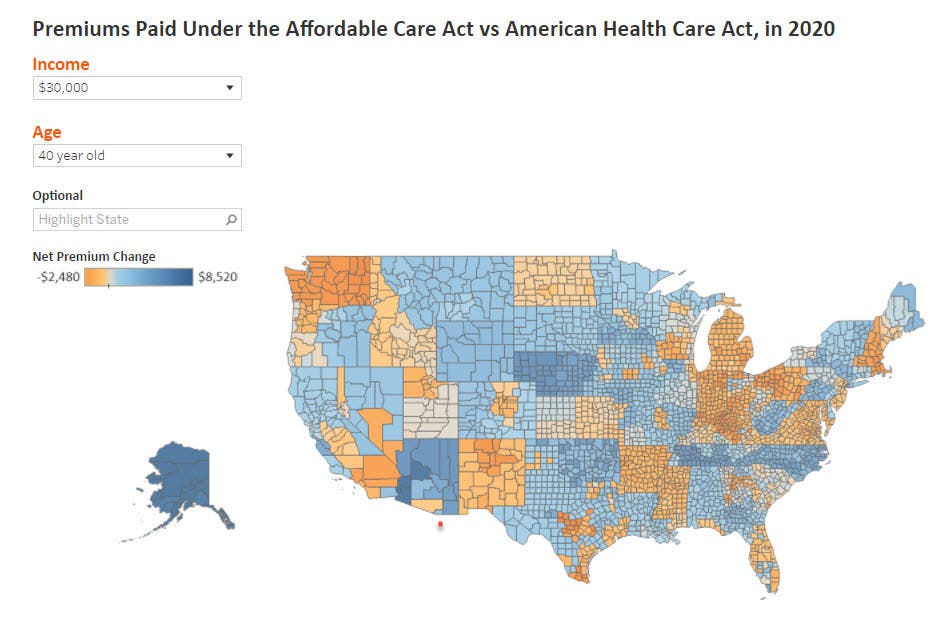

Consider the average changes using the value of 2017 dollars under an analysis by Kaiser Health News, an editorially independent program of the nonprofit Kaiser Family Foundation:

- Under current law, subsidies help those who earn up to $47, 520; under the Senate bill, subsidies would be cut entirely for those making over $41,58o;

- Current law requires most people who are given subsidies to pay from 2 percent to about 9.5 percent of their income on health care regardless of age; under the Senate bill, an age component would be introduced, requiring those ages 40-49 to pay up to 16.2 percent of their income.

- That means that a person making $41,580 would pay $5,197, under the Senate plan. That compares with $4,029 under current law.

- Things get worse for those who are older. Those 50-59 would pay $6,611 under the Senate plan compared to $4,029 currently. Those 60 and older would pay $6,735 compared to the current $4,029.

- Further, these figures are for insurance plans that would increase average deductibles from $3,500 to $6,000 and cover only 58 percent of costs compared to the current 70 percent.

- Those who make more than $41,58o are on their own.

- The out-of-pocket costs do not take into account drastic policy increases sure to be imposed on the elderly.

The non-partisan Congressional Budget Office said that the Senate's health care plan to replace Obamacare would increase the number of uninsured people by more than 15 million people compared with current law and 22 million people by 2026, according to an analysis released Monday.

The analysis is similar to the one CBO prepared for the House version of the health care bill passed in May. Under that bill, an estimated 23 million fewer Americans would have health care. While there would be one million fewer uninsured under the Senate legislation, it is likely that a disparate percentage of people losing their health care will be between the ages of 50 to 64, perhaps creating America’s next forgotten class. Many Americans in this age group are still reeling from the lost wages and career shifts forced upon them during America’s great recession of 2008.

The deep chasm between Republicans and Democrats over health care reflects the fundamental difference in the way the two parties perceive the role of government. Republicans generally favor a strict reading of the Constitution, which they believe intentionally limits the federal government from interfering in the daily lives of Americans and restricting their independence.

While that may frame the debate for leaders in each party, it is clear that the current GOP plan would fundamentally change the health care landscape across the country.

This has led to some raucous public debates in town meetings across the county, including one recently by Republican Sen. Deb Fischer, who faced a “a slew of boos and hisses” from her constituents, according to local news website LivewellNebraska.com based in Omaha.

“If you really want to do what we should, you take the existing law and you fix in a bipartisan way what needs to be done, and then you wouldn’t have people being worried — scared to death — that their health care was going to be taken away from them,” asserted Florida Sen. Bill Nelson in an interview with Patch in his Coral Gables office. “You wouldn’t have eruptions at all these town halls across the country that you see. People are speaking out because they’re scared.”

As Cody struggles to manage the many adjustments his medical conditions have brought his professional and personal life, he must also come to grips with a label that will follow him to his grave. Like millions of Americans who are transitioning from middle age into full-blown senior status, Cody has a preexisting condition and that makes him a bad insurance risk.

Americans between the ages of 50 to 64 age are people essentially born between the time President Dwight D. Eisenhower took his second oath of office, and the time the Green Bay Packers beat the Kansas City Chiefs to take Super Bowl I. They already have weathered America’s worst recession since the Great Stock Market Crash and many have been forced to live on their retirement savings. They are the sons and daughters of the Greatest Generation and they have lived through the Cold War, Watergate, disco, VCRs and texting.

Under Obamacare, people in Cody’s age group who are in the best of health and non smokers, now pay up to three times as much for health care as a younger person who has never been diagnosed with a chronic medical condition. About half of them receive government subsidies that pay for much of that cost.

But with the Republican replacement plans, older Americans would pay five times more for health insurance than what younger people pay — and the subsidies to help ease the financial burden would be cut.

Picture of Health

In the very near future, even those Americans who are the very picture of good health can expect to pay more for their health care — much more, according to health care experts at the non-partisan Kaiser Family Foundation, which has conducted an extensive analysis of the House replacement plan.“For some older people, especially those who live in high-cost areas, they could see premium increases that cost several thousands of dollars — in some cases even tens of thousands of dollars — per year,” declares Cynthia Cox, who conducts economic and policy research on health care costs in the United States for Kaiser.

About half of the middle-aged people who rely on Obamacare for their health care fall in the category of low-to-moderate income. Some would have been in that category before the recession, but many others were pushed into it during the unprecedented collapse of some of America’s most trusted financial institutions.

How will you fare under the House plan to replace Obamacare:

Gone would be the supplements that roughly half of the participants receive. In theory, a person who flips burgers at McDonald’s would pay the same premiums under the replacement plan as someone who makes twice as much, even up to $41,580.

“On top of that there could also be an even steeper premium increase if you are a sick older person,” said Cox, referring to states that drop Obamacare protections altogether. “So you not only have to pay five times what a younger person would pay, but you would also have to pay an additional part of your premium for whatever health condition you might have.”

Smokers will pay even more.

“If you are an old smoker who lives in a high-cost area, then you pay much more than five times more,” Cox said. “There’s compounding factors here.”

Everything Right

You would be hard pressed to find any compounding factors in the case of Ann Visser, a retired teacher, who recently celebrated her 60th birthday in the rural Iowa community of Pella. She is a non smoker who never experienced a significant medical event, and she exercises on most days.

“Three times a week we do fit for life with aerobics and weights,” Visser offered. “Then two times a week we do yoga. Two to three times a week I walk three miles with a friend.”

If there was one mistake she made, however, it was retiring from her job in the Pella Community School District in 2014 and opting to go on Obamacare.

“I really retired because I had met the love of my life and we thought we had a wonderful life ahead of us,” Visser shared. “The month after I put in for retirement, he was diagnosed with ALS — not quite how we wanted to see that all work out. I still thought I should retire because I thought that he would need care.

“By the next August, when it was time to go back to school, he passed away that month and I didn’t have a job to go back to because I had already put in for retirement. I lost two loves of my life in one month.”

But there was no going back and Visser had to prepare for the possibility of spending her golden years alone. She did the math and concluded that if she could save $200 a month by withdrawing from her school district’s health care plan and enrolling in Obamacare, that would be a prudent financial move.

“Now, three years later, I am faced with right now, no insurance — and no possibility of anyone who will sell it to me. There just isn’t anyone who has indicated that that can happen.”

The problem is that two of Iowa’s major health care players have already pulled out of the Obamacare marketplace and Visser is uncertain whether she will be able to arrange new coverage before she loses her existing plan on Dec. 31. Republicans insist that insurance companies are pulling out because the system is unsustainable while Democrats counter that the they are doing so over uncertainty as to whether the Trump administration will continue to fund the government insurance supplements.

“For 31 years I had a stellar record as far as my attendance, very few claims as far as insurance was concerned,” she recalled. “If you looked back on all that was paid in for me for insurance, and all that they had to pay out they made a lot of money on me and in the last three years they made a lot of me on me. I look at all of the money I have paid and now at age 60 — at the end of this year, I will have four years and four years until I am in Medicare.”

Much like Cody, who is anxious about his future, Visser doesn’t know if she will be able to find health care and whether she will be able to afford it if she does. She is already paying $700 per month to get coverage for herself with a $7,000 deductible.

“I think about that and I think ‘OK well I’ve been healthy. I maybe could be OK.’ Then, I think ‘OK well what happens if January of next year I’m diagnosed with cancer?’ I would use every cent of money I put aside for my retirement. And then where would I be? What would I do? So, it weighs very heavily on my mind about where I should look, what I should do.”

Feeling desperate, Visser recently contacted her former employer to ask if she could rejoin the health care plan. The response from the Pella Community School District was a simple no.

Time on Her Side

Yvonne Sadler doesn’t have to worry nearly as much in Madison, Wisconsin, where she is happy with her health care plan under Obamacare.

She pays a lot less than Visser and she has already turned 63 — only two years to go before she is safely aboard Medicare.

“I assume nothing’s going to happen yet for this calendar year,” she posited as to the earliest Obamacare might be replaced or premiums increase. “If they raise the prices as much as they say they could, I might just get by on savings.

Math of Despair

In its analysis of the replacement plan that passed the House, the Congressional Budget Office painted a grim picture of coverage for America, where 14 million more people than under current law would be uninsured in 2018 and 23 million more in a decade.

Here is how analysts arrived at their math of despair:

- Analysts calculated that the number of uninsured Americans would increase by 19 million in 2020 and 23 million in 2026 if the House bill becomes law.

- Adding those two numbers together, there would be a total of 51 million people under age 65 who would be uninsured. If Obamacare remains in place, only 28 million will lack health insurance, according to the analysis.

- Analysts concluded that only a few million people would use tax credits to purchase health care under the House plan, but the coverage would most likely be insufficient to cover major medical risks.

- In the 50 to 64 age group, the CBO predicted that single people who are on Obamacare and who earn more than $30,300 a year, would suffer an increase of the percentage of people who do not have health insurance — from 6.6 percent today to 11.2 percent.

- Single people making less than $30,300 a year would see an even larger increase from 11.7 percent of people in that group who lack health care to a whopping 29.9 percent, or three out of every 10 people.

Before Obamacare

Before doctors operated to remove the second toe on Cody’s right foot under Obamacare, he had two prior surgeries that he paid for out of his life savings.

Each one cost about $30,000. But an insurance policy would have cost him $40,000 per year — so he opted to roll the dice.

In contrast, Obamacare paid for almost all of the surgery in which his toe was removed.

“I am now someone with nine toes. But that experience only cost me a few hundred dollars,” Cody reasoned. “What I am afraid of is that under Trumpcare there is all kinds of nonsense about you’ll be able to keep your coverage but there is no guarantee that it will be affordable.”

The attorney became a first-time grandfather last year and Cody knows that his granddaughter will soon start asking questions about his foot.

“Hopefully, I’ll tell her that all grandpas only have nine toes if she ever sees and asks,” he said. “Hopefully, I won’t have to lower that number if we lose Obamacare and have to say ‘no, no all grandpas only have one foot.’”

A former trial attorney, Stephen Cody has already lost one of his toes and suffers from diminished vision. Photos by Paul Scicchitano.

Get more local news delivered straight to your inbox. Sign up for free Patch newsletters and alerts.