Business & Tech

Home Sales Statistics Don't Tell the Whole Story

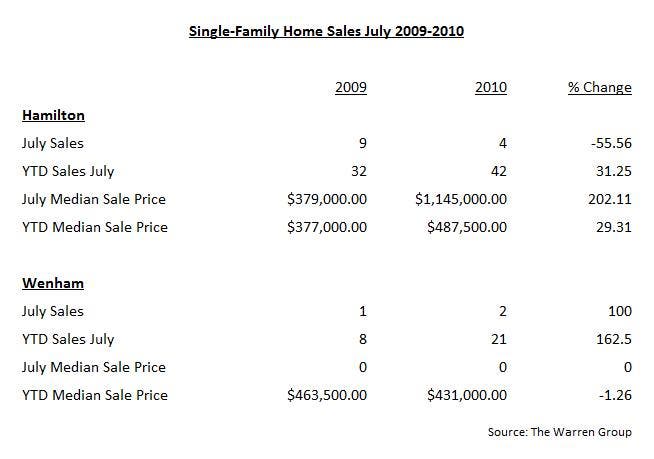

The Warren Group's July homes sales data shows prices down in Wenham and up in Hamilton, where it was fueled by two multi-million dollar sales.

Real estate statistics released last week don't fully explain a still sagging local real estate market, says a local Realtor.

The report, released on Aug. 31, by the Warren Group, a real estate and financial information firm, said July homes sales in the state dropped 26 percent but prices remained stable.

The statistics and story were disheartening for many local homeowners as their home is both the biggest purchase and largest investment they will ever make.

Find out what's happening in Hamilton-Wenhamfor free with the latest updates from Patch.

However, as with most things statistical, the numbers can tell more than one story. At first blush, the Warren report appears to show that Hamilton and Wenham have fared well over the past year.

In Wenham, home sales for July increased 100 percent from one home sale last year to two sales this year. Homes sales through July this year also increased by 162 percent with 21 sales this year as compared to eight sales last year.

Find out what's happening in Hamilton-Wenhamfor free with the latest updates from Patch.

The median sale prices this year to date dropped slightly from $463,500 compared to $431,000 this year.

In Hamilton, however, the Warren Group report shows that July home sales dropped 55.56 percent, from nine sales last year to four sales this year, although the median sale price jumped by a whopping 202 percent, from $379,000 to $1.145 million, a number driven by just two sales for more than $1 million.

But the first half of 2010 versus 2009 in Hamilton shows both the number of homes sales and the sale price increasing - home sales by 31 percent and prices by 29 percent.

Ronn Huth, owner of Buyer's Choice Realty in Wenham, said that considering the current economic conditions the local real estate numbers look OK on the surface, but don't tell the whole story.

"Interest rates are still low and with the market still down, there is a fair amount of inventory," he said, when asked how the market looked in general. "Properties are still moving well as long as sellers list their properties using good counsel."

And therein lies one big issue according to Huth - unrealistic expectations.

"If a seller bought in 2005 and is looking to sell now, they will not get what they paid for their property," he said.

Huth said that many sellers have trouble coming to terms with the market's downturn and are holding property longer, sometimes too long. That is why he advocates for sellers to have "good counsel" from a Realtor who has a realistic approach when deciding on a listing price for a home.

For example, Huth points to a house on Western Avenue that sold for $188,000 when it was priced at $199,900, but it had an original listing price of $314,900, a 40 percent reduction from the original listing price to the final sale price.

Another house on Highland Street recently sold for $160,000 when it was listed at $215,000, but had an original listing price of $309,000, a 48 percent reduction in price.

As further proof, Huth points to the sale of 25 Sagamore Farm Road where the list price was $1.995 million and the sale price was $1.655 million. However, the original list price, a price most people don't see, was $2.75 million, a 39 percent or $1.095 million reduction.

"This doesn't look like prices going up to me," Huth said. "Some believe that prices are going up, but I'm not convinced."

The now-expired $8,000 Home Buyer Tax Credit "got a lot more buyers out," but since it ended and the Making Home Affordable program was introduced, it has hurt, not helped, the market.

The Making Home Affordable program offers a cash incentive of up to $3,000 to homeowners on the brink of foreclosure to complete a short sale or deed in lieu of foreclosure. Further, it provides up to $6,000 to a loan provider for every short sale or deed in lieu they approve.

A short sale happens when the home owner owes more on the mortgage than the home's sale price will cover. For a short sale to process, the lender must agree to remove its lien despite the unpaid loan balance.

A deed in lieu of foreclosure is an agreement between a homeowner and mortgage company to avoid foreclosure where a delinquent homeowners signs the deed to their home over to their primary lender then walks away from the mortgage.

"I'm a little confused trying to see the benefit of this stimulus," he said, adding that the change in stimulus was intended to help with short sales. "Banks are just not being cooperative. For banks, foreclosures are just easier."

In the end, home sellers who can wait probably will and those who cannot will find price pressure and a competitive environment where buyers have a large inventory of homes to choose from. For their part, buyers will find tougher lending criteria and sellers who many times, because of financial pressure or mortgage commitments, cannot or will not negotiate.