Neighbor News

Newton's Pension Plan Problems Continue to Persist

Examining, Analyzing and Evaluating Newton's Unfunded Pension Liabilities, as well as addressing them without raising taxes and fees

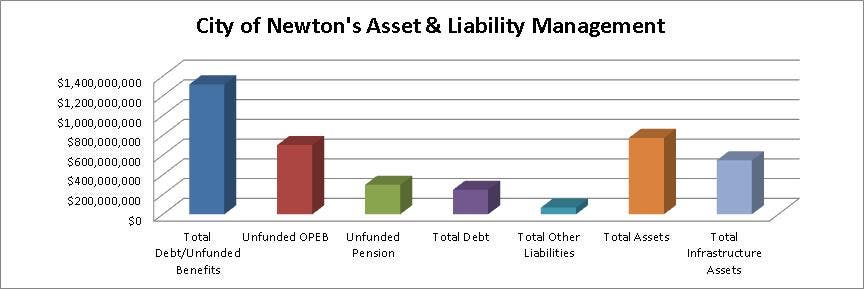

Did you know that The City of Newton owes $317 Million in unfunded pension liabilities? Unless you read the Actuarial Valuation Analysis Report Newton released last month for its Contributory Retirement System Pension Plan for calendar year 2015, you probably would not know this. When I last wrote about Newton’s pension woes three years ago [“Examining Potential Pension Woes”, August 14, 2013, page B3], Newton’s pension liability was $244 Million.

Despite Newton Mayor Setti Warren’s claims that he implemented a funding schedule fully funding Newton’s unfunded pension liability, the reality is that Newton’s unfunded pension liability increased from $208 Million when he took office to $317 Million as of 2016. Mayor Warren plans to “solve Newton’s pension deficit” by tripling Newton’s employer funded pension contributions over the next 13 years, from $21.7 Million in 2015 to $70.8 Million in 2028. We at the Newton Taxpayers Association do not think throwing more money into the pot will solve the pension system’s structural spending problem because you cannot solve a spending problem by throwing more money at it. We recommend that taxpayers guard their wallets because Newton government will try to gin up support for an override or debt exclusion over the next few years to bail out the underfunded pension plan.

Newton’s unfunded pension liability increased by 52% since Mayor Warren took office, versus 9.2% inflation growth and 4% population growth during this period. This was a surprise when one considers the following favorable headwinds that benefitted the pension plan since Mayor Warren took office:

Find out what's happening in Newtonfor free with the latest updates from Patch.

- Newton’s annual employer funded pension contribution increased by 56%.

- Newton’s annual employee funded pension contribution increased by 19%.

- The S&P 500 generated a total return of 107% because of the Federal Reserve’s easy money policies enabling companies to boost dividends and buyback their shares.

- The Barclays Aggregate Bond Index posted a 24% total return, benefitting from the Federal Reserve’s bond-buying activities.

- The Commonwealth of Massachusetts passed three pension reform laws from 2009 to 2011 in an attempt to control state and local pension costs.

In 2014, Mayor Warren announced that Newton fully fund its pension plan and retire its pension liability by Fiscal Year 2029. Once the pension plan was fully funded, Newton would then reallocate the excess annual pension contributions to funding the OPEB liability in the hopes of fully funding the OPEB plan and retiring the OPEB liability. As this was a huge leap forward relative to the minimum statewide requirement of full funding by 2040 and its previous internal funding deadline of 2037, we at the NTA wondered how Newton would achieve this lofty, almost utopian goal.

We understood that the Mayor wanted to increase pension contributions by 8.5% annually in 2014, but as Prop 2.5 limits tax levy growth to 2.5% plus new construction growth (which has averaged 1.5% annually over the last 33 years), we were wondering how Newton would be able to underwrite this initiative. We asked Mayor Warren how Newton would be able to achieve this objective, but he pawned us off on one of his mouthpieces who merely regurgitated what we already knew. We tried to explain to him that we already knew what Newton wanted to do, but we wanted to know HOW Newton would come up with the money, to which we got no reply. Due to the growth in pension benefit accruals and payments outpacing contributions and earnings, Warren was forced to increase the pension plan contribution growth rate from 8.5% in 2014 to 9.6% in 2016.

Find out what's happening in Newtonfor free with the latest updates from Patch.

Although Newton’s overall credit rating from the bond-rating agency Moody’s remains at Triple-A, its pension system liability is more in line with Single-A-rated communities. Newton’s adjusted unfunded liability represents 2.4% of its total tax base and 1.55X its adjusted operating revenue. According to Moody’s US Local Government General Obligation Rating Methodology, Moody’s gives a 10% weight to a community’s credit rating based on its pension system. Communities that have an adjusted pension liability that equals or exceeds 2.1% of its tax base and 0.8X its adjusted operating revenue earn a Single-A-rating from Moody’s for these two categories, which is applicable to Newton’s persistent pension plan woes.

Clearly, Newton’s pension plan suffers from the same structural spending problem afflicting the rest of Newton’s city government. Newton must reduce its compensation growth rate to 1% below revenue growth to change the trajectory of its pension plan liabilities and offset the 9.6% projected annual growth in city-funded pension contribution spending without burdening taxpayers with future override tax increases and new fees.