Community Corner

Living in Fairfield County & Watching Your Investments Tank

OUCH! The Gut Punch of Living in Fairfield County While Watching Your Investments Tank

This is a paid post contributed by a Patch Community Partner. The views expressed in this post are the author's own, and the information presented has not been verified by Patch.

It’s a crisp and colorful October morning, one of those rare days when everything seems to fall into place. The kids are off to school without much yelling today, the husband is happily doing his morning Wordle, and I have my sneakers on…ready to walk the dogs before I start the day’s work. I suggest a morning walk and my husband happily agrees, which leaves me with a bonus five minutes to check my computer while he gets ready.

I’m a Financial Advisor and Certified Divorce Financial Analyst, so of course I know the markets have been hit hard these last few months. I login to my personal account with a tiny grain of optimism, with the knowledge that my portfolio isn’t directly correlated to the major market indices. Deep breath. Is that number correct? Deeper breath. I look to the left of my keyboard and notice my giant electric bill where the delivery charges are more than double the actual electricity used (don’t get me started). The sprinkler system broke (again) as we discovered when our mini Bernadoodle came bounding into the house covered in mud. That’ll be another big chunk of change I can add to the groomer’s bill, given I have no time to spare to de-mud the dog. I opt not to login to my checking account because I know that just yesterday, we made another $500 grocery run!

I get pulled out of my computer coma by a cheerful, “Ready to walk the dogs? It’s a beautiful day!”

Oh right…the beautiful day. At this point I remind myself of what I know as a financial professional, and that is that markets move in both directions, and that I am invested for the long-term. I’m confident that I’ll eventually look back on these days with a contented smile, knowing I stayed the course. Another deep breath, and we’re off to walk in our lovely neighborhood, smiling and waving hello to our wonderful neighbors in our idyllic little Connecticut village.

I look at my neighbors out and about, also happily walking their kids to the bus, and wonder if they’ve recently logged into their IRA’s, brokerage accounts or 401k’s as well. Living in Fairfield County is expensive, and I wonder what could’ve been done differently, if anything, to avoid this recent gut punch. I’ve boiled it down to three key elements, and coincidentally they all start with “P” which makes for some nice alliteration.

- Perspective

- Planning

- Products

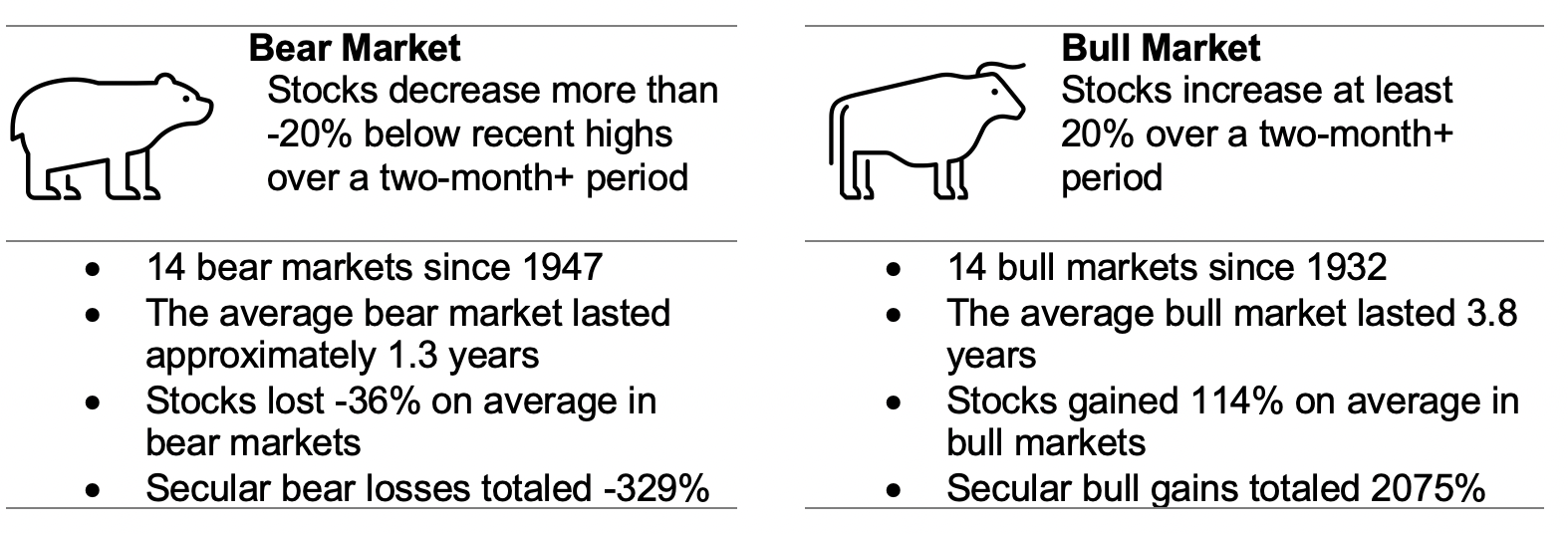

Perspective is the easy one. Well, it’s easy when the markets are going up, and I think sometimes we forget that we recently ended the longest bull market in history of 11 years (2009 – 2020). For perspective, between 1947 and 2022 there have been 14 bear markets, ranging in length from one month to 1.7 years. Today’s market is tough, and arguably the worst downturn we’ve seen since the financial crisis of 2008. If you want to talk about the “why”, we can talk about everything from inflation to interest rates, from unemployment and government spending to the US Dollar, continued covid lockdowns abroad, geopolitical turmoil, war in Ukraine, and a disrupted supply chain that impacts everyone’s earnings outlook. I’ve been discussing these types of factors with “the best of them” over the years, but here’s some perspective from my seat – anyone who tells you they know where the markets are heading in the next 1-3 years is not someone who should be giving investment advice.

PERSPECTIVE POINTS*

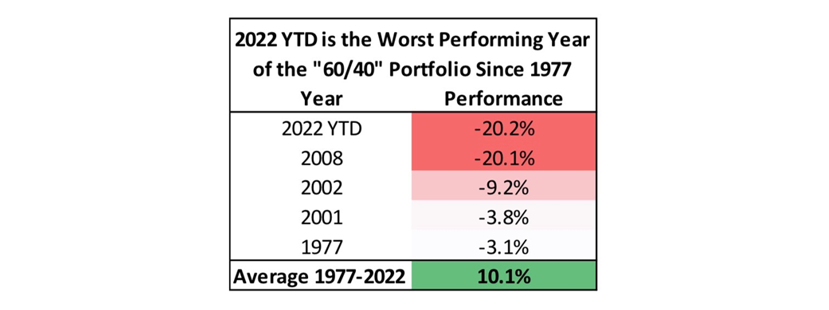

If this feels like the worst of times to you, you wouldn’t be wrong.

To date, 2022 is the worst performing year for both stocks and bonds since 1977.

But it’s important to remember that in that same period, the average annual return was still 10.1%. **

I have never been one to shy away from a strong opinion, but in today’s case, I see more variables at play now than ever before (making it exceptionally difficult to impossible to

predict,). The media seems to cover continued market weakness thoroughly, and I can’t disagree, but I can also make a solid case for exciting growth ahead. The first thing that comes to mind, is future growth fueled by pent up demand and suppressed supply. As one such example: car sales using cutting edge technologies, where demand is high and supply can’t keep pace, which has resulted in many earnings disappointments and extremely low market expectations in the near-term.

For my own personal investments, reviewing the potential market scenarios over the next 5, 10 and 20 years, provides context and perspective. After reflection I can report that I wouldn’t change a thing about my personal investments, even if it feels painful in the near term. That doesn’t mean that my personal investments are perfect; rather, that they’re appropriate for me at this stage of my life.

On the other hand, if I couldn’t recover from that initial gut punch of seeing my money drift downwards in the moment and was unable to shake it off and enjoy the day, I’d need to consider a new approach. For example, there are a lot of exciting products on the market today that can help to stabilize a portfolio amid the wild gyrations of today’s financial markets … but more on that later.

Planning

If you have felt gut punched in the last few months, as many of us have, without the knowledge or ability to put it in context and confidently move forward with your day, you need a better gameplan.

Financial planning is normally thought of as defining your goals, and fully inventorying your current and future income, assets, and liabilities. Sharing this information with your financial advisor enables them to help you develop an individualized investment portfolio in concert with your risk tolerance.

Today’s planning process, however, would fall short if it stopped there, as it wouldn’t have considered the impact of this year’s unanticipated events: hurricanes, war, inflation etc. The financial industry offers many other tools for your journey, beyond just real estate, stocks and bonds. A handful of years ago, that might have been sufficient, with one asset class offsetting another during vulnerable times in the market. In my opinion, that is no longer enough.

Products

Here’s the good news … after the financial debacle of 2008, many financial products are now subject to new and tighter regulations, mandatory disclosures, and greater transparency of information. Investment products are now being offered that can help to better minimize your downside risk. Annuities (not your grandmother’s anymore!), insurance

instruments, UIT’s (unit investment trusts) and even calculating the cash reserves needed to avoid having to lock in losses in a down cycle, offer alternative ways to diversify and protect, without throwing away the option for potential growth, and provide steady income when you need it most.

Living in Fairfield County is expensive. Without a plan to navigate these challenging times, years of progress can be lost in an instant. Finding a way to minimize losses and maximize growth, even when the headwinds are working against you, can be the difference between living with continued anxiety and fear, or enjoying each day with the confidence of knowing that you will get to the other side.

If you’d like to meet in person and talk about what this all means for you – feel free to reach out directly at Jen@waterwaywealthadvisors.com or join one of our next quarterly series meetings. Women & Money: A Quarterly Series

Footnotes:

Bloomberg, Lincoln Financial Group. Bear markets are defined as instances of at least a 20% market decline.

2 Source for bear/bull market stats is Ned Davis Research as of 12/15/21, unless otherwise noted.

Source for bull/bear market time periods First Trust Advisors, Bloomberg

Source for P/E ratio history Schiller index

** Bloomberg

Securities offered through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC. Investment Advisory Services offered through Kestra Advisory Services, LLC (KAS), an affiliate of Kestra IS. Westchester Benefit Group, Inc. is not affiliated with Kestra IS or Kestra AS. Investor Disclosures: https://www.kestrafinancial.com/disclosures

This post is an advertorial piece contributed by a Patch Community Partner, a local brand partner. To learn more, click here.