Community Corner

Options for Closing Budget Shortfall

A response to Mayor Sandack's request for ideas on the budget.

The Village Council continues to move forward on the Fiscal Year 2011 budget. At the Oct. 12 village council meeting, Mayor Ron Sandack repeated his request for ideas on the budget.

This is the presentation I made to council on Oct. 19. It is part of the podcast recording on the village website (starting at 33:24). I presented some ideas that do not entail new taxes or new borrowing, but which might reduce the need to raise taxes moving forward by bridging the revenue gap—if they can be done.

Option #1 The Ogden TIF preamble agreement

Find out what's happening in Downers Grovefor free with the latest updates from Patch.

The preamble agreement between the village and Grade School District 58 was written in 2001. From the language of the agreement, it appeared that DG staff anticipated another round of heavy borrowing upfront to kick start redevelopment. Instead then-Deputy-Village-Manager and TIF Administrator Dave Fieldman chose to move to a PAYGO model, and the TIF has built a surplus instead, forward funding projects and avoiding interest costs.

"Section 4 Agreement Re-openers" of the preamble agreement outlines conditions under which talks "will" occur to renegotiate the agreement itself. Item B, Puffer Hefty being brought into the district, is one condition that has been met.

Find out what's happening in Downers Grovefor free with the latest updates from Patch.

The State laws governing TIF districts strictly prohibit agreements with single districts. The DG/58 preamble agreement was designed to skirt that law. By eliminating the agreement and replacing it with a legal revenue sharing agreement that is accounted for and reported within the TIF financials annually, minor tax relief would be extended to all residential and commercial property owners for the 14 remaining years of the TIF district.

Organizing the Ogden TIF Fund, so that 50% of the increment is designated to ongoing project funds and the other half is annually declared a surplus:

- Provides for the payments in the preamble agreement to 58.

- Reserves a growing fund for redevelopment.

- Relieves part of the hidden tax on residents and businesses that TIF districts represent.

The net result would be to eliminate an annual $135,000+ payment out of the general fund, and create an annual payment of ~ $54,000+ into the general fund, a net gain of $189,000 and growing yearly.

Option #2 Declare the surplus for the Ogden TIF

This would provide the Village with a one time fix of their share of the built up increment, over $391,000 dollars. To get it, by law everyone else gets their proportional share, and ~$1,875,000 would be divided between the two school districts.

After the one-time declaration, the Ogden TIF would still be generating ~$800,000 annually, and growing, unless the surplus is declared and paid in full or in part each year. OASIS, a redevelopment matching fund program featured in another story here on the DGPatch, remains untouched and fully funded to help accelerate making Ogden a better commercial artery.

Option #3 Tapping cash balances

Since 2004 Cash Balances of some funds have steadily increased. FY11 the Parking Deck Fund has $964,797. Using $170,000 stills leaves more than a 6 month expense only operating reserve (doesn't count revenues that offset costs), and be 60% above the fund cash balances five years ago, during better economic times.

The Library board has independent budget authority. They would need to agree to spend down the cash balance by applying it to this years' request, or come to next years' budget using fund balances to reduce their levy request. With new board members and a soon to be new Library Director, it might either be tricky, or an opportune time to consider tapping cash balances to provide property taxpayers with some relief.

A $200,000 draw down to $2,900,000, keeps the fund well over 540% higher than 5 years ago, when they were just above $530,000. The $2,800,000 remaining in this fund represents an almost 8 month expense-only operating reserve (revenues are not counted). The Library construction fund (FY11 cash balance $164,785) or the Library debt service fund (FY11 cash balance $857,061) are separate funds not included.

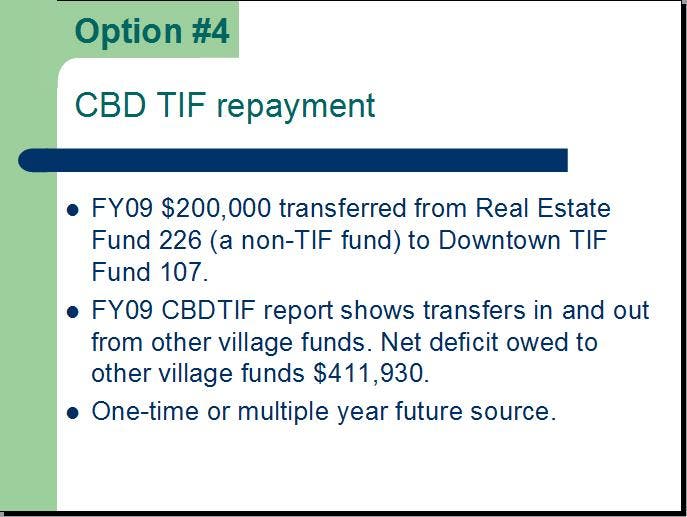

Option #4 Downtown TIF repayment

Put simply, the CBD TIF district fund pays back the various village funds.

In FY09, $200,000 was transferred from Real Estate Fund 226 (a non-TIF fund) to Downtown TIF Fund 107. Additionally, the same year Downtown TIF Annual Report documents transfers in and out from other village funds that created a net deficit potentially owed back to the General Fund of $411,930.

Even if the $200,000-$611,930 were budgeted to be repaid, the CBD TIF fund cannot repay this in one lump sum payment; it would need to be spread out over multiple years.

Option #5 Policy change on CBD TIF surpluses

Cash flows for the CBD TIF will turn positive starting this year. 80 condos at Acadia on the Green appear for the first time on the 2009 tax roles, with tax payments totaling ~$379,099.30 appearing on 2010 tax rolls. These CBD condos are in an SSA area that funds the Downtown Management Group. If it enhances the coffers, perhaps the DMG can share costs of the $45,000 parking study that directly benefits the CBD.

Maybe, just maybe, the extra funds could help fund a community based event, such as a community themed heritage festival that could be held in the early summer. It might be popular.

The Downtown TIF has debt payments scheduled out to 2021, increasing each year.

The total borrowed principal, $34,435,000, was money spent on DG, rebuilding the downtown and adding the parking deck. Interest only payments on that debt, $10,781,443, are money not spent on DG needs. The total, $45,216,443, represents 44.3% of village total debt.

What was asked for last week from council was budget options. These options represent change, change in the way tax dollars are booked and budgeted. As to specific ways to use these revenues, council would have to act on them first, then decide how they will be used.

My singular request was that any fiscal budget assistance, which might come out of council and staff adopting any of these strategies, be used to reduce the local government portion of the real estate tax bill to residents and businesses of Downers Grove.

Mayor Sandack and staff said they will look into it, and see if they can do anything along these lines. Residents will have additional meetings to hear and have their say, but the budget process is wrapping up. The next Village Council meeting is 7 p.m., Tuesday, Nov. 2.