Health & Fitness

Considering an FHA Loan? Act Now.

Evanston Realtor Scott Kelly shares about important changes in FHA's Mortgage Insurance Premium policies that can save you money.

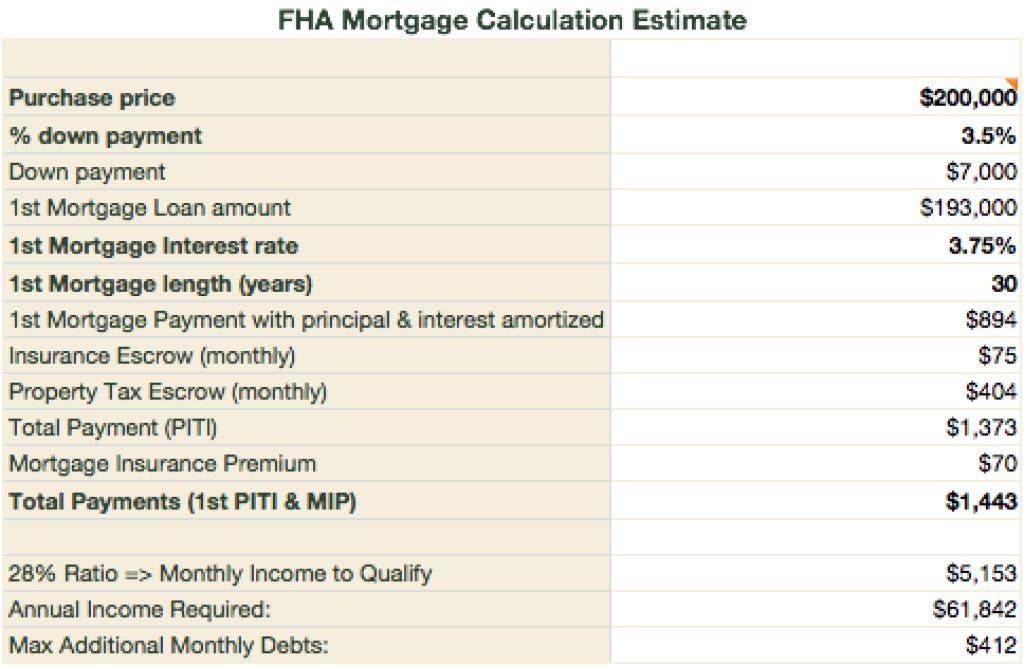

If you are a potential home-buyer considering an FHA loan to purchase a home by using a down payment that is less than 20% of the purchase price, now is your time to act. Here’s why: The FHA recently announced significant changes to the Mortgage Insurance Premium policies related to these low down payment mortgage products. Click here for all the details straight from the Department of Housing and Urban Development. The bottom line is this: Instead of mortgage insurance premiums expiring when the homeowners equity increases to greater than 22% of the property value, the mortgage insurance premiums never expire and instead continue throughout the entire term of the loan. This is a significant change in the total borrowing costs of an FHA mortgage. Consider the following example of a $200,000 home purchase and review the numbers in the attached chart.

For the next few months, FHA borrowers will be able to borrow under the old rules. But the FHA’s new policies mean that future FHA borrowers will be paying Mortgage Insurance Premiums for many more years than they would have otherwise. In the example in the chart, the increased costs to borrowers would be $21,000 over the life of the loan ($70 per month x 12 months x 25 years).

Now is the time to act if you want to use an FHA loan to buy your next home with as little as a 3.5% down payment. Let’s talk. Let’s go do some housing for good. Visit my site at Baird & Warner today and register there for a market summary that includes a daily list of homes that meet your search criteria.