Politics & Government

North Suburban Property Tax Bills Will Rise 6.5 Percent

The Cook County Clerk released 2016 tax rates for each of the county's more than 1,400 taxing bodies Tuesday.

In the final step before property tax bills are mailed out, the Cook County Clerk's office released the complete 2016 property tax rates for each of the county's more than 1,400 taxing agencies.

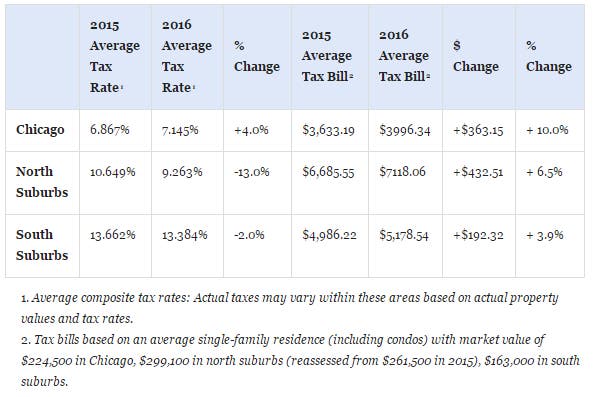

North suburban homeowners in Cook County can expect to see their bills rise by an average of 6.5 percent this year. That equates to an extra $432.51 on the average bill (which currently totals about $7,000 per year), according to figured released Tuesday by the Clerk's office.

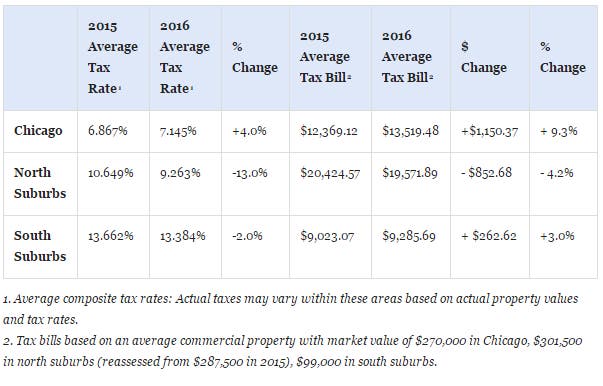

Commercial property tax in Northern Cook County is a different story. The average commercial bill is expected to decline by 4.2 percent, dropping by $852.68.

Find out what's happening in Glenviewfor free with the latest updates from Patch.

In the South suburbs, rates will rise an average of just 3.9 percent, while the average residential taxpayer in the City of Chicago can expect to see the largest increase to their bill, roughly 10 percent, according to the Cook County Clerk.

Due August 1, tax bills are calculated based on the amount of money sought from all applicable taxing districts (the levy), the property’s assessed value, the state equalization factor (a multiplier to provide uniformity to assessments) and the applicable tax rate.(Sign up for our free breaking news alerts and newsletters for your community.)

Find out what's happening in Glenviewfor free with the latest updates from Patch.

» Read the Full 2016 Tax Rate Report (via Cook County Clerk)

Property Tax Changes for Average Single Family Dwellings by Region

Property Tax Changes for Average Commercial Properties by Region

For the second year in a row, the total of all taxes extended for all taxing districts in Cook County exceeds $13 billion. Last year the total tax billed in Cook County was $13.1 billion. This year the total tax in Cook County is $13.7 billion. The City of Chicago’s extension again exceeds $1 billion, an 8.5 percent increase over last year.

Total 2016 Taxes Billed in Cook County by Region

TAXABLE VALUE

Property assessments in Cook County are set by the Cook County Assessor and finalized by the Cook County Board of Review. These assessments are equalized by the Illinois Department of Revenue (IDOR) in order to ensure uniform assessment state-wide. This equalized assessed value, less applicable exemptions, is the taxable value for property.

The overall equalized assessed value (EAV) in Cook County increased by 8.1 percent this year, largely due to the reassessment of the Northern Suburbs which saw assessed values in the northern suburbs increase 11.9% on average. When added to a 5% increase in the equalizer, taxable values in the northern suburbs increased an average of 17.4%. The City of Chicago and the Southern Suburbs, which were not reassessed this year, saw increases in EAV of 4.3%, primarily due to the increase in the equalizer.

2016 Equalized Assessed Values (EAVs) in Cook County by Region

Impact of Value on Tax Rates

Due to the lower property value base in the Southern Suburbs, property owners typically see higher tax rates than those in the City or the Northern Suburbs which have a larger taxable value base. Taxing districts such as schools and municipalities still must provide services which are funded by property taxes regardless of this difference in value. As a result, tax rates tend to be significantly higher in the more depressed areas of the County. For example the highest tax rate in Cook County is found in the Village of Ford Heights where property owners pay a tax that is nearly 40% of their taxable value, compared to property owners in the City of Chicago or the Northern Suburbs where the tax bill in some cases is approximately 7% of taxable value.

As Clerk Orr previously indicated, “property taxes are inherently regressive and disproportionately impact people in poorer regions. The overreliance on this mechanism of funding local government compounds existing inequities.” Clerk Orr has consistently called on the state to adopt a fair income tax that allows less reliance on property taxes and renders taxes more equitable for all.

Tax Rate Calculation

Tax rates are calculated by dividing the amount of money each taxing district has requested in their levy by the total taxable value within each district. A taxing agency or district is a body of government such as a school district, library, or municipality, which levies real estate taxes. The tax rates of all districts that service a particular property are added to create the composite tax rate applicable to each property.

City of Chicago Increases

Typically, when EAVs increase, taxpayers will see a corresponding reduction in tax rates. City of Chicago taxpayers, however, are seeing rates increase, due in large part to increased levies from the Chicago Board of Education and the City of Chicago itself. The City of Chicago increased its levy by $109 million this year as part of a planned four-year property tax increase which began last year. Additionally, the State Legislature approved a $272 million CPS levy increase to pay for teachers’ pensions which took effect this year. As a result, homeowners in the City of Chicago should expect to see their tax bills increase 10.0 percent on average.

Lowest Composite Tax Rate

For the first time since tax year 2008, the lowest composite tax rate in Cook County is not in the City of Chicago. Some taxpayers in the Village of Barrington may now claim that distinction. The City of Chicago’s general composite rate is still the lowest on average of all municipalities in Cook County, but some taxpayers in parts of the northern suburbs will see lower rates than City taxpayers.

PTELL

The Property Tax Extension Limitation Law (PTELL), also known as the “Tax Cap Law” limits the increase in revenue that qualifying districts may collect to the rate of inflation. In most cases, districts this year were limited to an increase equal to the 2016 Consumer Price Index (CPI) of 0.7 percent, the second-lowest increase since the Tax Cap Law began over 20 years ago. Home rule districts, debt obligations, other special purpose funds, and value derived from new property and terminated Tax Increment Financing Districts (TIFs) are exempt from this limitation. Next year, the CPI will limit tax revenues to an increase of 2.1 percent.

Transit TIF

This year, for the first time, the City of Chicago has created a Tax Increment Financing District (TIF) to help fund public transit improvements. This “Transit TIF” is different from other TIFs in that it is not required to demonstrate “blight”, is allowed to run for up to 35 years instead of the typical 23 years, and part of its incremental revenue will be returned to the taxing districts, including CPS. With the addition of this TIF, which is one-mile-wide and extends from North Avenue to Devon Avenue along the Red and Purple CTA train lines, 1 in 4 properties in the City of Chicago are now in TIF. The Clerk will have additional information about TIFs and Transit TIFs available in July.

» via the Office of the Cook County Clerk

Get more local news delivered straight to your inbox. Sign up for free Patch newsletters and alerts.