Politics & Government

Lake Forest Explains Changes To Its Pension Funding Formula

The city hiked contributions this year, aiming to cut future increases and cover a $42 million unfunded liability in public safety pensions.

From The City of Lake Forest: Throughout the nation and most notably Illinois, communities are grappling with their public pension programs. Lake Forest is no exception, and as public officials, the City Council believes it is essential to continue to provide a frank and open dialogue with the community about the current status of our three pension programs and their potential impact on our community, not only today but for years to come.

The City has three pension systems: 1) the Illinois Municipal Retirement Fund (IMRF), which is a pension fund for City staff who are not part of the two public safety pension funds, which are 2) the Police Pension Fund and 3) the Fire Pension Fund. While local pension boards manage the Police and Fire pension funds, the IMRF is governed by a statewide board elected by plan participants. We do not include other State pensions here, such as our school district or County plans, as the City Council does not have the responsibility to fund them.

Moreover, most of the terms of the funds, including eligibility for participation, rates of contribution, terms of benefits, and the percentage of investments that can be allocated in a specific sector are mandated by State Statute. These regulations mean that the City of Lake Forest has no input on the plan benefits, investment policy, management or any other terms of these funds.

Find out what's happening in Lake Forest-Lake Blufffor free with the latest updates from Patch.

The pension plans are funded from three sources, 1) member contributions (9% of compensation), 2) fund investment returns, and 3) annual City contributions. State Statutes currently require police and fire pension plans to achieve 90 percent funding by 2040. We do not believe that this requirement will be sustainable for most Illinois municipalities. Previous State-imposed funding deadlines of 2020 and 2033 have been extended, now to 2040, and a similar extension beyond 2040 is anticipated. Such extensions only serve to defer the inevitable, and the City Council is choosing to explore alternative fiscally sustainable models that will not only meet, but exceed, State requirements.

A variety of assumptions are used to calculate annual funding requirements, such as investment returns, mortality and future salary increases. At present, employers are required to make minimum contributions as provided by certified actuaries to meet a target of 90 percent funding by 2040. The actuarial assumptions used in determining the minimum contributions are one of the few factors within the City’s control.

Find out what's happening in Lake Forest-Lake Blufffor free with the latest updates from Patch.

As of April 30, 2018, the City’s IMRF plan is funded at 98.83%, the Fire Pension Fund is funded at 70.64%, and the Police Pension Fund is funded at 54.20 % (Click here to view annual pension fund investment returns).

In actual figures, the Police Pension Fund (at 4/30/2018) has current assets of $31,650,935 and an actuarial accrued liability of $58,400,246, leaving an unfunded liability of $26,749,311. The Fire Pension Fund (as of 4/30/2018) has current assets of $36,256,485 and an actuarial accrued liability of $51,327,313, leaving an unfunded liability of $15,070,828. The combined total actuarial unfunded liability for the two funds is $41,820,139.

While the City historically has always made at least the state minimum required contributions, several factors have contributed to the current funding levels. It is important to note the State of Illinois mandates all benefits Police and Fire employees are to receive, and in what amount, and for how many years of service.. The City has no control in these matters. Further, pension liabilities increase due to the increased life expectancy of retirees over the years, which increases the anticipated costs under current valuations. Secondly, investments have not always achieved the actuarially assumed rate of return. Thirdly, retirees receiving benefits are entitled to a 3% annual cost of living increase, which for many years exceeded the rate of inflation. Thus, the cost of living benefit has a significant compounding effect on unfunded pension liabilities. Finally, the State legislature has adopted benefit enhancements, which apply retroactively, without providing the revenue for funding the enhancements.

The City Council recently changed the City’s approach to managing our future pension fund contributions. For the current fiscal year, the City significantly altered the actuarial assumptions to amortize the unfunded liability at an accelerated pace. The change necessitated an increase in current year funding by approximately $800,000 but was designed to reduce average annual increases in funding going forward. Also, the City is engaged in discussions with its independent actuary to phase in an open "rolling 15-year" funding model. The new plan will potentially enable Lake Forest to achieve 80% funding of the Police and Fire Pension Fund in the 2034-2035 period while keeping our annual contributions level over many years into the future.

The Illinois State Constitution includes a clause guaranteeing pension benefits. The Illinois Supreme Court has repeatedly upheld that clause, basically stating that prior and current workers are guaranteed the benefits promised to them, and those benefits may not be diminished in any way. Consequently, unless there is a constitutional amendment, all municipalities, must operate under the assumption that meeting the current pension obligation must be achieved.

Other communities’ experiences highlight the potential consequences of not adequately addressing funding percentages and allowing them to decrease. Local press reported that Danville, Illinois Police and Fire pension funds recently fell to 17 percent and 30 percent funding respectively, and forcing Danville to implement double-digit increases to their property taxes and an almost 200 percent increase in their public pension safety fee on all parcels of property to meet their obligations.

In April, Chicago media reported that the city of Harvey, Illinois, laid off over 30 firefighters and police officers to pay for a court-mandated payment to pension funds that the city had failed to adequately fund over the years, resulting in the fire fund falling to a level of 27 percent funding. The public safety unions in Harvey appealed to Springfield about the shortage, and the Comptroller withheld $1.4MM in revenue due to Harvey from the state to satisfy the deficit, prompting the layoffs. Also, the Peoria City Council reportedly voted a few weeks ago to eliminate 22 fire and 18 police positions to fill a $6 million budget hole and is contemplating a per parcel public safety pension fee to address increasing pension costs.

In Lake Forest, the City will contribute a combined total of more than $4.2 million in the current fiscal year to fund the Police and Fire pensions. $3.6M of that funding will come from property taxes, while the remaining $.6M will come from the City’s public safety pension fee, billed quarterly on residents’ utility bills. The public safety pension fee was adopted in Fiscal Year 2018, and increased in Fiscal Year 2019, to raise public awareness of the pension funding issues faced by municipal employers.

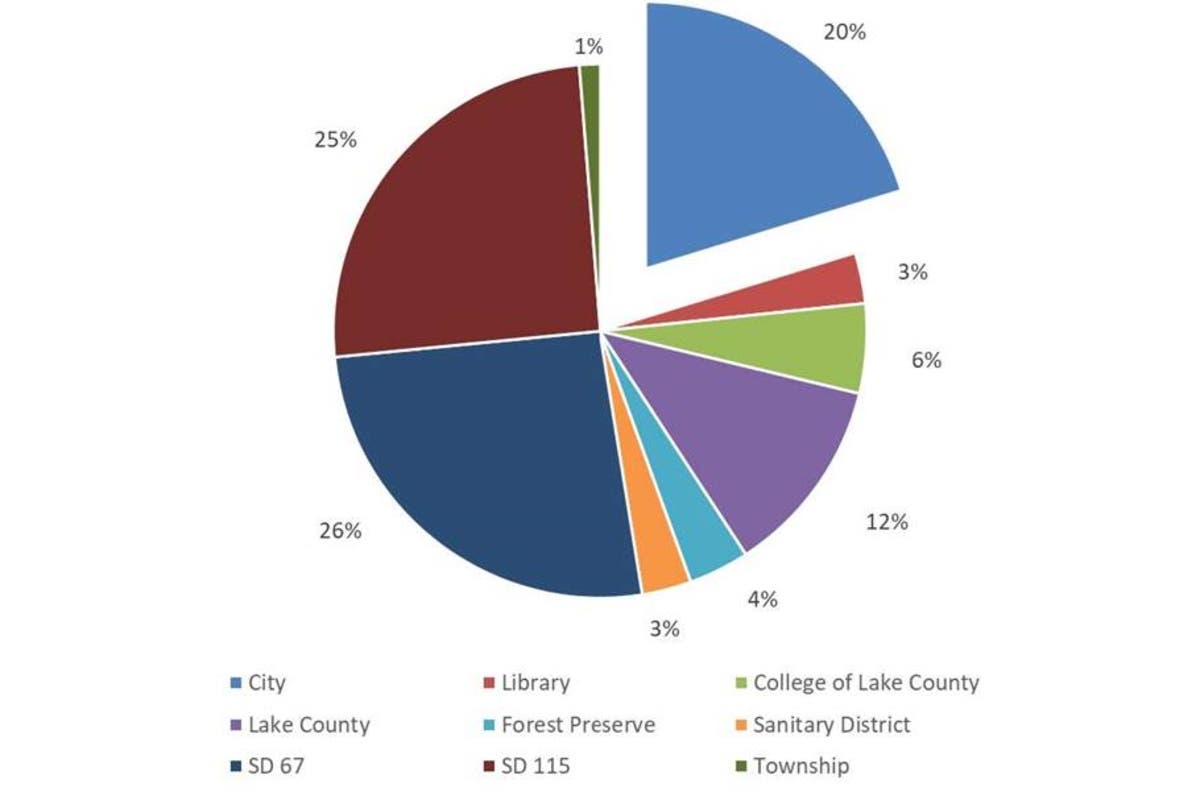

The total property tax levy for the city last year was $31.3 million. Lake Forest residents pay the lowest overall property tax rate in Lake County. We intend to try to maintain that status. A resident’s property tax bill is comprised of 9 separate taxing bodies, with the City representing 20% of the total tax bill (see graph at top of letter).

To honor our public safety pension funding commitment, the City undertakes an annual independent actuarial study of our Police and Fire pension obligations to calculate both the minimum contribution under State Statute and the recommended contribution to meet the City’s Pension Funding Policy. As part of that study, the City explores potential revisions to the Pension Funding Policy to ensure that the City’s approach continues to both meet legal requirements and be fiscally sustainable over the long-term.

Recently, it was determined that by removing the 2040 funding target and moving to an open, continuous 15-year rolling plan, we could achieve 80% funding in a reasonable number of years. More importantly, we found that Lake Forest can gradually reach and then maintain a level annual City pension contribution far into the future while keeping an 80% funded status. Should we continue with the State-mandated 2040 funding target, our annual pension contributions will increase dramatically over the period from 2019 to 2040 and then will fall to a minimal level after 2040.

In our opinion, a phased-in open 15-year rolling amortization pension plan is fiscally sustainable and fairer for the current and future residents. It will leave future contributions more stable over time and provide residents in the period after 2040 with a reasonable pension contribution for our future City Police and Fire employees. Current Police and Fire employees are assured that the City’s contribution has met, and in most future years, will exceed state requirements.

We believe our actuarial-based public safety pension funding model for Lake Forest is fiscally responsible, both for meeting our current and future Police and Fire pension obligations and for meeting all of our other City services obligations.

More pension information may be found here on the City's website.

Image via The City of Lake Forest