Business & Tech

Credit Card Debt Grows In Texas, U.S.

Among $16 billion on plastic nationwide, Austin posts biggest credit card balance increase in the U.S. Check to see how your city fares.

AUSTIN, TEXAS — With the expense of Christmas holidays just two weeks away, a pair of new study offers more sobering analysis on Americans' credit card debt — including Texas. It's not pretty: Americans racked up $16 billion in such indebtedness, with several Texas cities among those with least sustainable credit card debt.

The findings are among those found on the personal-finance website WalletHub Q3 2018 Credit Card Debt Study, which analyzed credit card debt nationwide from June through September. In a separate but similar study, CompareCards.com found that Austin had the biggest credit card balance in increase in the entire nation — a 12.3 percent spike from September 2017 to September 2018.

Austin stands out in WalletHub the report, ranking among the nation's top five major cities with the most debt on consumer credit cards. The capital city ranked fifth rarefied list, and rounding out the top five were Boston; Washington, D.C.; New York City; and Denver.

Find out what's happening in Austinfor free with the latest updates from Patch.

The findings show the $16 billion in collective credit card debt represents an all-time record level for a third quarter ever. As a result, another Federal Reserve rate hike — which economists predict has a 70 percent chance of happening on Dec. 19 — would now cost credit card users an extra $1.56 billion in interest, the study's analysts found.

Related story: Austin 'Cost To Live Comfortably' Increase Is Highest In Nation

Find out what's happening in Austinfor free with the latest updates from Patch.

While the debt picture is worrisome nationwide, analysts noted, some areas have bigger payment problems than others according to WalletHub’s report on the Cities with the Most & Least Credit Card Debt. WalletHub’s researchers drew upon data from TransUnion, the Federal Reserve, the U.S. Census Bureau and WalletHub’s proprietary credit card payoff calculator to determine the cost and time required to repay the median credit card balance in more than 2,500 U.S. cities.

One Texas city was among the list of those with least sustainable debt. Consumers in the Dallas suburb of Colleyville were found to have a median debt load of $5,593. The cost to pay that debt off is $880, analysts found, and it would take 24 months and 28 days — the nation's longest debt payoff timeline. The city is among many in the 99th percentile nationally, which denotes areas with the least-sustainable credit card debt.

Also in the 99 percentile club was The Woodlands in the Houston area. There, the median credit card debt was found to be $5,088, with a cost of $670 to pay off. The amount of time for payoff: 20 months and 27 days

At the other end of the debt spectrum, some Texas cities were placed among those with most sustainable debt. Take Gainesville, Texas, for example, landing in the 1 percentile. The median debt load of $2,428 costs a merre $45 to pay off in 2 months and 14 days, according to researchers. Similarly, the Dallas suburb of Allen was in the 1 percentile, with a median debt of $3,780 taking $95 to pay in a mere 3 months and 16 days.

Read the full WalletHub report by clicking here.

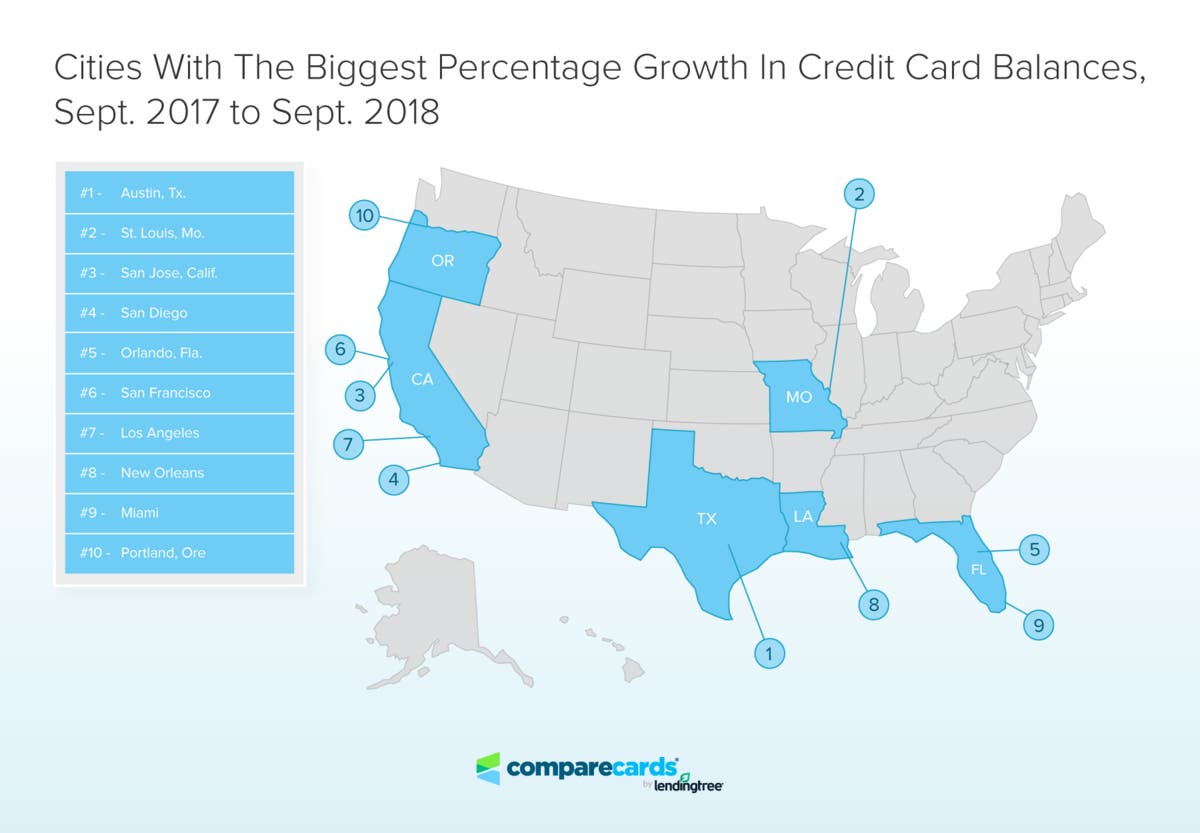

Another similar study also casts a not-too-flattering spotlight on Austin as it relates to credit card debt. According to CompareCards.com, the capital city had the biggest credit card balance increase in the U.S. in the past year. The average credit card balance in Austin jumped 12 percent from September 2017 to September 2018, researchers found. That's pretty high, considering credit card balances grew an average of 3.6 percent in the nation's 50 largest cities in the U.S. during the same studied time period.

Last year, the average credit card balance in Austin was $6,165, according to the CompareCards.com study. Last year, researchers found that average debt grew to $6,924 — an increase of 12.3 percent. That's the biggest credit card balance Increase in the entire U.S.

"Austin may be a victim of its own success," said Matt Schulz, Chief Industry Analyst at CompareCards. "As the city has grown rapidly in recent years, it has also become a much more expensive place to live, so many Austinites may be leaning a little more heavily on credit cards these days."

Map via CompareCards.com

Dallas-Fort Worth and Houston fared better in the CompareCards study, ranked 33rd and 36th, respectively. In the former, credit card debt grew by a modest 2.2 percent to $6,238 from $6,105 in a one-year period as of September. The average credit card balance in Houston increased to a smaller during the studied time period to $6,184 from $6,110 for a 1.2 percent jump.

CompareCards used a statistically relevant sampling of anonymized My LendingTree user data, comparing information from September 2017 with data from September 2018. (My LendingTree user credit information is provided by TransUnion.) The data includes only active, revolving bank cards with a balance. CompareCards also relied on Census Bureau data to determine the 50 largest metropolitan areas in the U.S.

To read the full CompareCards report, click here.

In the WalletHub study, users can input the name of a city for a credit card debt snapshot. This feature offers something of a guide in determining how personal debt compares to median credit card debt loads. The WalletHub study also includes a credit card calculator for consumers to figure out how long it might take to pay off ttheir debt.

WalletHub researchers crunched the numbers for snapshots into other cities' credit card debt, including a number of Texas cities. Here's how other cities fared:

ARLINGTON

Percentile: 65

Median credit card debt: $2,520

Cost to pay off: $219

Months and days until payoff: 13 months and 19 days

AUSTIN

Percentile: 92

Median credit card debt: $3,217

Cost to pay off: $331

Months and days until payoff: 16 months, 6 days

CEDAR PARK

Percentile: 98

Median credit card debt: $3,967

Cost to pay off: $459

Months and days until payoff: 18 months and 8 days

COPPELL

Percentile: 98

Median credit card debt: $4,141

Cost to pay off: $484

Months and days until payoff: 18 months and 14 days

DALLAS

Percentile: 73

Median credit card debt: $2,893

Cost to pay off: $261

Months and days until payoff: 14 months and 4 days

DEL RIO

Percentile: 29

Median credit card debt: $2,173

Cost to pay off: $164

Months and days until payoff: 11 months and 26 days

EL PASO

Percentile: 65

Median credit card debt: $2,577

Cost to pay off: $223

Months and days until payoff: 13 months and 19 days

HARLINGEN

Percentile: 58

Median credit card debt: $2,472

Cost to pay off: $209

Months and days until payoff: 13 months and 8 days

IRVING

Percentile: 59

Median credit card debt: $2,267

Cost to pay off: $193

Months and days until payoff: 13 months and 9 days

LAREDO

Percentile: 62

Median credit card debt: $2,384

Cost to pay off: $204

Months and days until payoff: 13 months and 13 days

LEANDER

Percentile: 95

Median credit card debt: $3,715

Cost to pay off: $396

Months and days until payoff: 16 months and 26 days

MCALLEN

Percentile: 48

Median credit card debt: $2,483

Cost to pay off: $201

Months and days until payoff: 12 months and 21 days

PASADENA

Percentile: 11

Median credit card debt: $1,800

Cost to pay off: $123

Months and days until payoff: 10 months and 20 day

PFLUGERVILLE

Percentile: 83

Median credit card debt: $3,178

Cost to pay off: $305

Months and days until payoff: 15 months and 2 days

PLANO

Percentile: 88

Median credit card debt: $3,241

Cost to pay off: $319

Months and days until payoff: 15 months and 16 days

ROUND ROCK

Percentile: 92

Median credit card debt: $3,390

Cost to pay off: $348

Months and days until payoff: 16 months and 4 days

SAN ANTONIO

Percentile: 73

Median credit card debt: $2,809

Cost to pay off: $254

Months and days until payoff: 14 months and 5 days

SPRING

Percentile: 94

Median credit card debt: $3,715

Cost to pay off: $393

Months and days until payoff: 16 months and 21 days

SUGAR LAND

Percentile: 88

Median credit card debt: $3,395

Cost to pay off: $335

Months and days until payoff: 15 months and 16 days

WACO

Percentile: 20

Median credit card debt: $2,229

Cost to pay off: $162

Months and days until payoff: 11 months and 8 days

THE WOODLANDS

Percentile: 99

Median credit card debt: $5,088

Cost to pay off: $670

Months and days until payoff: 20 months and 27 days

Yes, some of those are scary stats. But there are steps consumers can take to lower down their credit card debt in a methodical manner. CompareCards.com offers the following advice:

- Consolidate credit debt with a 0% intro APR balance transfer card: Fighting credit card debt by getting another credit card may seem counterintuitive, but used wisely, these cards can dramatically reduce the amount of interest you pay and shorten your payoff time. Just make sure that you understand the fees and other details associated with the card before you apply. Finally and most importantly, make sure that you don’t just see the new card and all that available credit as an excuse to run up more debt. Read our guide on consolidating debt with a balance transfer.

- Call your card issuer and ask for a lower interest rate: You’d be shocked how often this works. Nearly two-thirds of those who asked for a lower APR got one, according to a recent CompareCards.com survey, and the average reported reduction was 5.5 percentage points. That’s a really big deal. For example, if you have a $5,000 balance on a card with a 24% APR and pay $150 per month on the card, you’ll pay $3,322 in interest and take 56 months to pay off that card. Drop that APR by 5.5 percentage points to 18.5% and you’ll pay just $2,072 in interest and pay it off in 48 months. That’s a savings of $1,250 and eight months. And you don’t have to have perfect credit to have your request granted. Pick up the phone. It can’t hurt to ask.

- Make a budget (or revisit your old one): You can’t make a serious plan to tackle debt unless you know exactly how much money is coming in and going out of your household each month. If you’ve never made a budget, take time to create one. Write down everything you spend, and all of your income. It’ll allow you to determine whether you need to focus on reducing spending or increasing income – or most likely some of both. And if you have a budget but haven’t reviewed it in a while, do it. Budgets are living, breathing things. Those numbers that you came up with in 2016 or 2017 may no longer apply.

- Get your credit in shape: Poor credit costs you a fortune. It’s as simple as that. That’s why it’s so important to keep your credit score in good shape. One of the best moves you can make: checking your credit report. If you haven’t done it in a long time, do it today. Millions of Americans have errors on their credit reports that are artificially holding their scores down. Don’t let that be you. Check your report and make sure all of the accounts listed are actually yours and all of the negative information on it (if any) is actually legitimate. If something looks amiss, follow the credit bureau’s instructions on their website for how to report the error. It can make a difference.

Get Patch's Daily Newsletters and Real Time Alerts

>>> Photo by ESB Professional/Shutterstock

Get more local news delivered straight to your inbox. Sign up for free Patch newsletters and alerts.