Neighbor News

Solving Newton's $700+ Million OPEB Problem

How to solve Newton's $700 Million OPEB Liability without raising taxes or cutting programs we all support

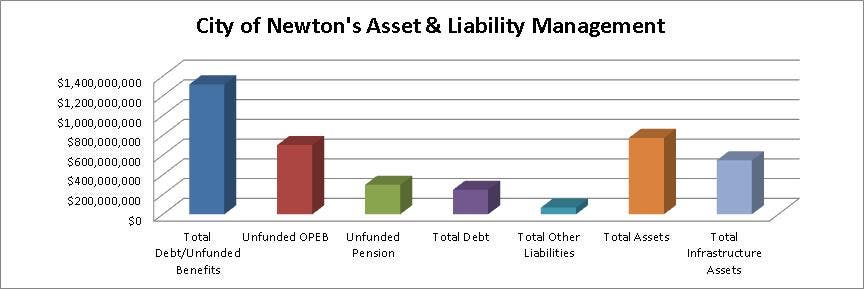

Nearly three years ago, I analyzed Newton’s underfunded pension plan woes [“Examining Potential Pension Woes”, August 14, 2013 page B3]. Newton’s net unfunded pension plan liability was $244 Million as of when I wrote my column and is $298.7 Million now. Did you know that Newton’s accrued Other Than Pension Post-Retirement Employee Benefits (OPEB) liability is now $701.5 million as of the end of Fiscal Year 2015 (assuming a 2.04% discount rate associated with underfunded plans)? Even if one assumes a 7.04% discount rate normally associated with fully funded plans, Newton’s accrued OPEB obligation balance is still $319 million. This represents $10,000-$22,000 per household that Newton taxpayers are on the hook for in addition to their quarterly tax bills. What people do not know is Newton’s projected OPEB liability is over $1.1 billion ($34,375 per household).

Although all municipalities are struggling with unfunded OPEB liabilities, Newton’s OPEB liabilities are shockingly high relative to a well-managed community like Hingham. After further review, Hingham’s OPEB management is significantly stronger than Newton’s for the following reasons:

· Hingham began funding its OPEB liabilities in 2009 (without resorting to override tax increases like Wellesley) versus 2011 for Newton and has nearly four times the OPEB assets ($9 million) versus Newton ($2.1 Million)

Find out what's happening in Newtonfor free with the latest updates from Patch.

· Hingham’s employees pay 50% of the insurance premium for their health insurance versus 20%-30% for Newton employees

· Hingham’s net OPEB liability is $50.5 million, versus $319-$701.5 million for Newton

Find out what's happening in Newtonfor free with the latest updates from Patch.

· Hingham’s net adjusted OPEB liability per household is $6,135, versus $10,000-$22,000 for Newton

· We at the Newton Taxpayers Association think Newton should follow Hingham’s lead on reforming OPEB, rather than dismissing them as “not our peer community”.

Newton’s Financial Audit Advisory Committee met in April one month after the override passed in 2013. The Committee recommended that Newton should start a public education campaign regarding these liabilities, as did Tom Sheff. A recent aldermanic report on OPEB suggested that if Newton “Prefunds the OPEB costs, it will need a marketing strategy to help residents understand.” We at the NTA interpret this to mean that Newton wants to gin up support for another override tax increase to fund these OPEB liabilities.

In addition, Newton’s credit rating firm wants a concrete plan to address the OPEB liabilities because Newton’s OPEB Liability has increased from $531.7 Million in 2010 to $701.5 Million in 2015. Yes, Newton’s OPEB Obligation increased by $170 Million during Mayor Warren’s administration despite his rosy rhetoric regarding how he plans to solve the pension and OPEB issue. Fortunately for Newton’s taxpayers, the NTA has a five-point plan available that solves Newton’s OPEB problem without raising taxes through Proposition 2.5 overrides or cutting popular programs, projects and services:

1. Newton reduces the health insurance subsidy from 80% (70%-75% for employees hired after FY 2011) to 50% for all employees/retirees. This results in $16 million of annual savings, provides a health insurance subsidy in line with what the private sector pays its employees/retirees and should be negotiated as part of any new union contracts.

2. Enacting point 1 reduces the OPEB obligation from $701.5 million to $441 million

3. Newton invests those savings for 11 years in the Commonwealth of Massachusetts's PRIT Core Fund (same investment trust fund Newton currently invests its pension and OPEB trust assets)

4. Newton earns an average annual return of 7.04% on those assets resulting in gross projected assets of $302 million after the end of 11 years.

We believe that 7% is a reasonable average annual return considering that low-risk regulated utilities are guaranteed a 10% annual return on equity by their regulators and the PRIT fund is primarily invested in industries that have higher expected returns on capital than utilities.

5. Enacting point 4 enables Newton to increase the discount rate used to value OPEB liabilities from 2.04% to 7.04%, reduces the OPEB obligation’s present value from $441 Million to $202 Million and provides a $100 million buffer for any investment earnings shortfalls and additional OPEB obligation benefit accruals.

The NTA concludes that Newton has a structural spending problem concerning its OPEB plan. The problem with OPEB is that it gives the employee a defined benefit and saddles Newton with an undefined cost. It’s absolute lunacy to deal with that structure. It has got to go away, forever, fast! Newton needs to do more work going forward and the NTA’s proposed solution must be the lynchpin of any OPEB reform in Newton. Newton has $774 million in gross assets to cover $1 billion in net underfunded pension/OPEB liabilities and $248 million in debt ($1.25 billion in total interest incurring liabilities) and the NTA opposes future override tax increases that fund lavish retiree benefits for government unions when private sector workers no longer get these benefits.